When Payments Stopped Pulsating

When Payments Stopped Pulsating

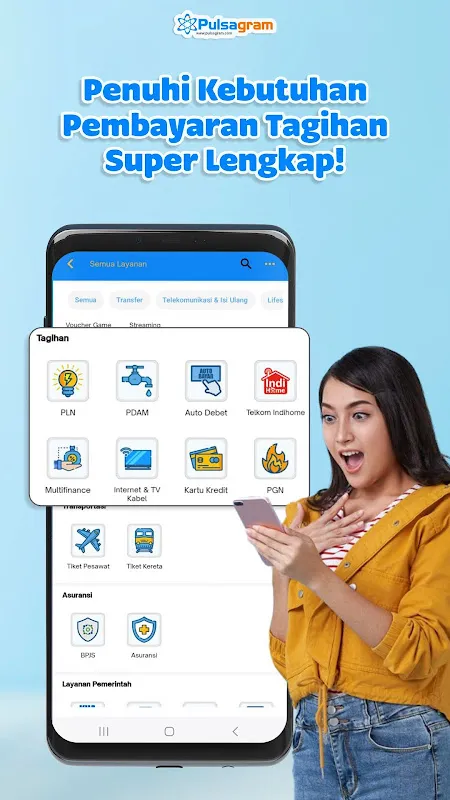

My knuckles went white around the phone as the "Transaction Failed" notification mocked me for the third time. Sweat traced cold paths down my temples while the cafe owner’s impatient stare bored into my skull. Somewhere between juggling supplier invoices and my daughter’s forgotten lunch money, my digital wallet had flatlined. That’s when I finally surrendered to the neon green icon I’d been side-eyeing for weeks – Pulsagram.

The first sync felt like defusing a bomb. Initial Detonation Business accounts snarled with personal subscriptions, PayPal balances hid like shy ghosts, and three different banking apps demanded separate sacrificial rituals just to check balances. Pulsagram didn’t just organize them; it *understood* the chaos. With biometric trembling, I granted access. Seconds later, the app performed financial necromancy – resurrecting all 27 payment methods I’d buried across platforms. My café humiliation ended with a fingerprint tap so fluid, the espresso machine still hissed louder than the transaction.

Real magic struck at midnight invoices. Midnight Mercantile Crouched over lukewarm tea, I faced a Slovakian freelancer’s invoice demanding payment through some obscure local gateway. Pre-Pulsagram, this meant currency conversion acrobatics, wire transfer forms written in hieroglyphics, and 48 hours of prayer. Now? A search for "Slovak Instant Transfer," a direct API handshake between Pulsagram and Bratislava’s banking backend I never knew existed, and confirmation vibrated through my phone before steam stopped rising from my mug. The app didn’t just pay; it whispered secrets about regional payment rails only fintech veterans could decode.

But friction finds cracks. Last Tuesday, euphoria curdled during a pop-up vendor market. My artisan candle merchant beamed, holding up her QR sticker like a trophy. Pulsagram scanned it, whirred thoughtfully, then declared: "Payment Network Unsupported." Her smile faltered. That tiny vendor used a hyper-local African payment processor Pulsagram’s mighty aggregation hadn’t swallowed yet. I fumbled for crumpled cash, the app’s failure a sour tang beneath the bergamot-scented air. Later, rage-typing feedback felt cathartic – how dare this pocket Leviathan miss one fish?

Yet habit rewires you. Yesterday, panic spiked when my accounting software screamed about duplicate payments. Instead of the usual forensic spreadsheet dig, I swiped open Pulsagram’s reconciliation dashboard. There it was – two identical coffee machine payments glaring red. Deeper dive revealed the culprit: my bank’s archaic system had double-sent the authorization. Reconciliation Revelation Pulsagram didn’t just spot the error; it visualized the payment’s entire journey – from tap to merchant settlement – with timestamped nodes. Seeing the real-time settlement latency explained the ghost payment. Resolution? One tap dispute, automated evidence packet sent. The refund hit before my panic did.

It’s not love; it’s a tense symbiosis. Pulsagram demands absolute financial transparency – every account, every card, every digital IOU. In return, it gifts surreal clarity: watching money flow globally from my couch feels like playing god with ledgers. But when it stumbles? Like discovering your cyborg heart skipped a beat. Tonight, paying a Tokyo-based designer, I watch yen convert at rates beating my bank’s, the app quietly leveraging its aggregated volume for bulk FX advantage. Yet I still eye QR codes warily, wondering if today’s the day it chokes on some obscure protocol. That tension? That’s the pulse. Never entirely steady, but fiercely, indispensably alive.

Keywords:Pulsagram Mobile,news,fintech revolution,payment anxiety,business finance