Cardboard Boxes and Crimson Icons

Cardboard Boxes and Crimson Icons

Rain lashed against my studio apartment window that Tuesday evening, the sound drowning out the microwave's hum as I reheated dollar-store noodles for the third night running. My phone buzzed - another bank notification. I braced myself before looking, fingers trembling slightly as I swiped up. Overdraft fee. Again. That sinking feeling hit like a physical blow, my stomach knotting as I stared at the negative balance glowing in merciless digital red. The radiator hissed mockingly while I mentally calculated which utility bill to delay this month. Financial dread had become my unwelcome roommate, its cold breath fogging every decision.

Thursday brought the breaking point. At the grocery checkout, my debit card declined with that soft, shameful beep. "Insufficient funds." The cashier's pitying glance as I abandoned essentials felt like a paper cut to the soul. Walking home empty-handed through slushy streets, I passed a bus shelter plastered with credit card ads - gleaming teeth and tropical beaches taunting my reality. That's when I noticed it: a tiny graffiti tag near the ad's corner. Someone had spray-painted a crimson V over the model's perfect smile, stark and urgent as a warning label.

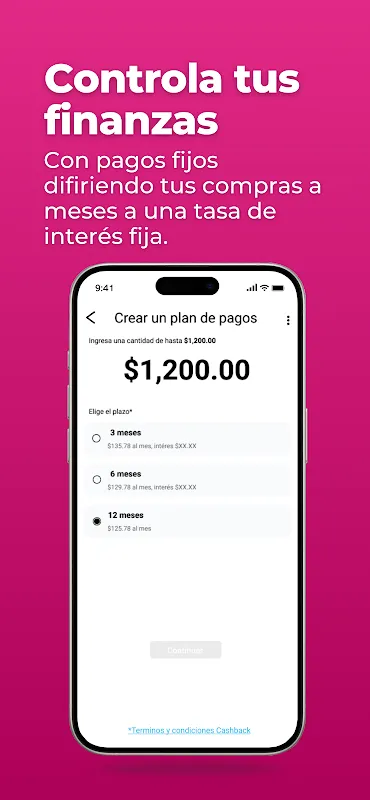

The image haunted me. Later, curled on my thrift-store couch with cracked phone screen glowing, I typed "V crimson card" into the app store. Vexi's icon appeared - that same bloody red V against matte black, looking less like corporate branding and more like a rebel insignia. What hooked me wasn't the promises ("ZERO FEES" flashed boldly), but the installation size: a mere 37MB. Most financial apps felt like bloated surveillance tools, but this downloaded in seconds. My cracked screen didn't distort its minimalist interface - just a clean timeline of circular progress trackers where other apps buried you in menus.

Setup felt unnervingly human. Instead of demanding pay stubs or social security digits upfront, it asked two questions: "What's one money goal that keeps you awake?" (I typed: "Not flinching at checkout lines") and "What small expense brings you joy?" (My answer: "Used bookshop paperbacks"). This psychological handshake mattered - the app seemed to acknowledge money as emotional before treating it as mathematical. When it finally requested banking access, I held my breath granting permissions. Most apps vacuum your transaction history into black-box algorithms, but Vexi's Real-Time Ledger Sync worked differently. Using banking API protocols with end-to-end encryption, it created what felt like a glass-walled vault - I could literally watch its algorithm categorize my $4.29 coffee as it happened, no mysterious "processing" delays.

Then came the test. Payday arrived, but so did an unexpected dental bill devouring 80% of my funds. Old habits screamed: borrow from Peter to pay Paul. Instead, I opened Vexi's "Breathing Room" feature - not a loan, but a dynamic cashflow reorganizer. It analyzed my calendar (dentist Thursday, rent due Friday) and recurring subscriptions (that forgotten gym membership draining $29.99 monthly). Using predictive scheduling, it proposed shifting my phone bill cycle by three days and cancelling two dormant services. The cashback activated automatically - $14 credited instantly from partnered vendors when I approved the changes. Not life-changing money, but enough for groceries without the overdraft dance. The relief tasted sweeter than any luxury dessert.

Six weeks later, I noticed the shift. Not just in my account (still lean, but no longer hemorrhaging), but in my body. Shoulders didn't tense when checking balances. I bought a paperback guilt-free with cashback rewards, savoring the bookstore's dusty scent. The real magic? How Vexi weaponized micro-behavior. Every time I avoided impulse buys, its "Progress Pulse" feature vibrated gently - not a notification, but a tactile reward. One evening, analyzing my spending clusters, I discovered a pattern: emotional purchases spiked near my toxic ex's birthday. The app didn't judge; its "Trigger Alerts" simply asked: "Set a reminder for next month?" Turning financial ghosts into manageable data points felt like therapy.

Yesterday, rain returned. But this time, I ordered takeout without checking my bank app first. The confidence startled me - not from sudden wealth, but from Vexi's radical transparency. Its open-source budgeting framework meant I understood exactly how interest calculations worked when I tested its credit-building tools. Unlike traditional cards with predatory APR structures, Vexi's system uses cascading micro-loans secured against your cashback earnings. Approval isn't based on ancient credit scores, but real-time fiscal behavior. When I qualified for a $50 credit line, I celebrated not the amount, but the algorithm recognizing eight weeks of punctual $5 repayments. My financial dignity, pixel by pixel, restored.

The crimson V on my home screen now feels like a lifeline carved in kevlar, not a corporate logo. It hasn't made me rich. But tonight, eating proper dinner during the downpour, I realize what it truly offers: the luxury of predictability. No more adrenaline spikes at checkout counters. Just clean numbers, honest algorithms, and the quiet certainty that next week's noodles will be by choice, not necessity.

Keywords:Vexi,news,financial anxiety,open banking,behavioral economics