CoolCredit: My Financial Phoenix

CoolCredit: My Financial Phoenix

Rain lashed against the coffee shop window as I stared at the rejection email - another auto loan application denied. My palms left sweaty smudges on the phone screen where the number 592 glared back, a scarlet letter in digital form. That three-digit curse followed me everywhere: whispering behind landlords' polite declines, shouting from credit card denial letters, even lurking in the awkward silence when friends discussed home equity. I was drowning in a sea of past financial mistakes - a maxed-out emergency card here, a forgotten student loan payment there - each misstep fossilized in my credit report like geological layers of shame.

When I first opened CoolCredit, skepticism curdled my stomach. Another app promising miracles? But within minutes, its interface sliced through my cynicism. Unlike other platforms showing static numbers, it visualized my credit health as a pulsing ecosystem - utilization ratios breathing like living organisms, payment histories flowing like rivers, with real-time alerts flashing when hard inquiries stabbed through the landscape. That first night, I fell down a rabbit hole analyzing how different scoring models weighed each factor. FICO 8 punished late payments like a vengeful god while VantageScore 4.0 showed surprising leniency toward medical collections - arcane knowledge suddenly made tactile through color-coded impact sliders.

The true revelation came when disputing an erroneous collections account. CoolCredit didn't just provide template letters - it generated dispute narratives tailored to each bureau's quirks. TransUnion required surgical precision with account numbers formatted EXACTLY right, while Experian responded better to narrative flourishes. When I uploaded evidence, the app's OCR technology extracted relevant dates and amounts before I could blink, auto-populating fields with frightening accuracy. Three weeks later, watching that $1,200 phantom debt evaporate felt like shedding concrete shoes.

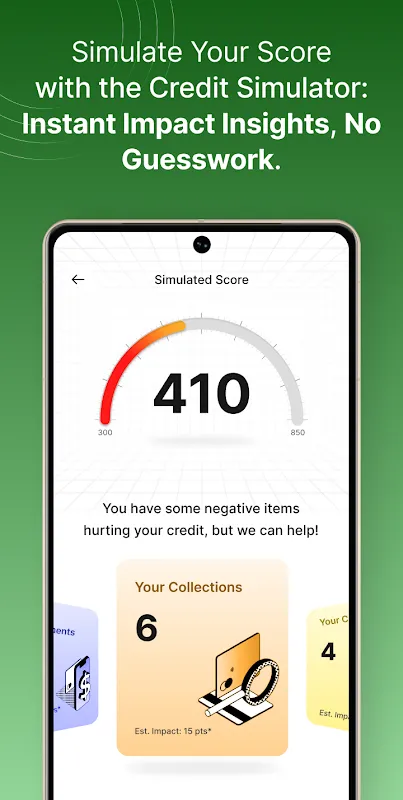

But the app's real genius lived in its predictive brutality. That Thursday evening when I almost applied for a department store card to get 15% off a sofa? CoolCredit's simulator projected an instant 8-point drop. "Inquiry sensitivity threshold exceeded" flashed in crimson, with an explanation of how new accounts temporarily lower average account age. I canceled the application, bought secondhand, and weeks later watched my score climb precisely as predicted when I paid down a high-balance card instead. This wasn't magic - it was cold, beautiful mathematics made visceral.

Yet for all its algorithmic brilliance, the human moments stung deepest. That Saturday morning notification: "Credit limit increased by $500 on Chase Freedom." Normally cause for celebration, it triggered panic - higher limits meant greater temptation. I nearly uninstalled right there. But CoolCredit anticipated this too. Its behavioral nudge system suggested freezing the card physically in a block of ice while auto-paying $25 monthly to maintain activity. The absurd physicality of chiseling at a frozen credit card became my ritual whenever temptation struck.

Ninety days in, the transformation felt surreal. Where credit karma once showed jagged cliffs of despair, CoolCredit revealed topography I could navigate. I learned to time credit checks like a surfer reading swells - applying for apartments during mid-cycle reporting periods when utilization dipped lowest. When my FICO finally pierced 700, the celebration felt anticlimactic. The real victory was understanding why: how AZEO (all zero except one) methodology boosted me 17 points overnight by strategically leaving $5 on one card. Financial literacy stopped being abstraction and became muscle memory.

Does it frustrate? God yes. The app's obsession with perfection borders on pathological. It once shamed me for a 2% utilization spike from buying groceries. And their security paranoia means fingerprint login fails if your thumb's slightly damp - I've screamed at my phone in a downpour more than once. But these irritations pale when balanced against liberation. Yesterday, I got pre-approved for a mortgage. Not subprime garbage, but honest-to-god 4.5% fixed. As the loan officer rattled off terms, I wasn't just hearing numbers - I understood the exact sequence of financial decisions that made them possible. That knowledge, more than any score, is what CoolCredit truly gave me. My financial phoenix didn't just rise from ashes - it taught me fire prevention.

Keywords:CoolCredit,news,credit rehabilitation,financial behavior,scoring algorithms