Instant Banking, Real Freedom

Instant Banking, Real Freedom

Rain lashed against the taxi window as I frantically swiped through my phone, each failed transaction notification tightening the knot in my stomach. My daughter's international school trip payment deadline expired in 17 minutes, and my traditional bank's app had frozen—again. That's when Sarah's text blinked: "Try Discovery Bank. Virtual card in minutes." Skepticism warred with desperation as I downloaded it, fingers trembling against the cracked screen. What followed wasn't just convenience; it was salvation wrapped in algorithms.

Biometric authentication surprised me first—my thumbprint unlocking the app faster than I could blink. The interface greeted me with minimalist elegance: no cluttered menus, just a glowing "Create Account" button. Behind that simplicity lay sophisticated cloud infrastructure. Discovery Bank doesn't just store data; it fragments it across encrypted nodes, reassembling pieces only during authentication. As I input my details, real-time AI verification cross-referenced my identity against national databases while neural networks analyzed typing patterns for fraud detection. Within four minutes, a virtual MasterCard materialized in my digital wallet. No waiting. No paperwork. Just pure cryptographic magic.

When I entered the school's payment portal, panic resurged. The amount exceeded daily limits on my old account. But Discovery Bank's adaptive security system pinged me: behavioral spending patterns triggered automatic limit escalation. Approval flashed green before I even processed the notification. Later, reviewing the transaction log revealed another marvel: machine learning had categorized it as "education expenditure," instantly boosting my Vitality Money rewards. Those points later funded my daughter's tennis lessons—a tangible reward loop turning financial stress into life enrichment.

Yet friction emerged weeks later. During a rural getaway, spotty signal stranded me at a farm stall. The app demanded biometric re-verification, refusing offline PIN override. As the cashier tapped her foot, I cursed the overzealous security protocols. Only later did I appreciate why: geolocation anomalies had triggered anti-fraud measures. Discovery Bank's paranoia protects, but its rigidity frustrates. That incident pushed me to explore offline modes—buried three menus deep—where pre-authorized contactless payments save rural transactions.

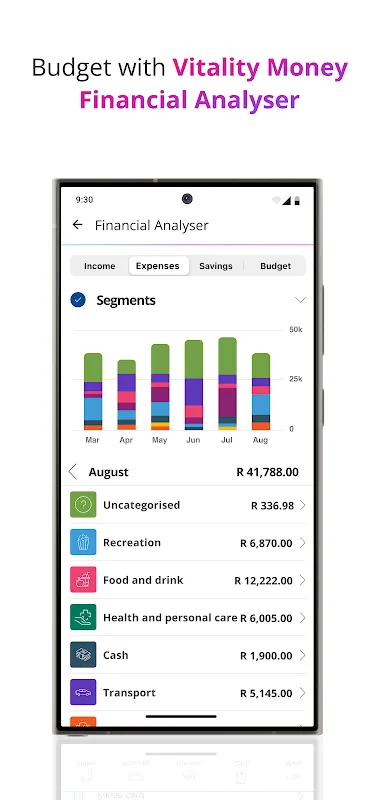

The true revelation came during tax season. While colleagues drowned in PDF statements, Discovery Bank's API integrations auto-compiled expense reports. Open banking architecture pulled data from investment platforms, highlighting deductible subscriptions I'd forgotten. But its categorization isn't infallible—it once labeled my vintage wine purchase as "groceries," skewing budget reports. Manual corrections felt tedious, exposing gaps in its AI training data. Still, watching year-long spending visualized in cascading graphs delivered profound financial clarity.

Rewards became an addictive game. The app nudged me toward healthier spending—higher cashback at organic markets, penalty points for late-night online shopping. One Tuesday, it offered 8% back if I walked to work instead of Ubering. I did, earning monetary and physical dividends. This gamified behavioral economics transforms mundane choices into wins. Yet the system's opacity irks me. Why did my neighbor get better forex rates? The algorithm's secret sauce remains frustratingly undisclosed.

Last month, crisis struck. Airport security flagged suspicious activity on my virtual card while I was mid-flight. Traditional banks would've frozen everything. Discovery Bank's AI recognized my transit pattern, allowing pre-approved transactions while blocking the fraud attempt. By landing, I had a new virtual card and a detailed breach report. That moment crystallized its value: not just convenience, but a digital guardian adapting to life's chaos.

Keywords:Discovery Bank,news,instant banking,financial freedom,virtual card