Marbles: My Money Lifesaver

Marbles: My Money Lifesaver

I remember the day vividly; I was at a trendy café with colleagues, celebrating a project completion. The bill came, and as usual, we decided to split it. My heart raced as I fumbled through my wallet, pulling out three different cards, each with uncertain balances. The embarrassment was palpable—I had to ask the waiter to wait while I checked my banking app, which took forever to load. That moment of panic, surrounded by laughing friends, made me realize how out of control my finances were. I wasn't just disorganized; I was drowning in a sea of transactions, with no lifeline in sight.

Later that evening, fueled by frustration, I scoured the app store for something, anything, that could help. That's when I stumbled upon Marbles Card. The description promised clarity and control, and I downloaded it with a mix of hope and skepticism. Setting it up was my first hurdle; linking my bank accounts felt invasive, and I worried about security. But the app's assurance of end-to-end encryption and use of tokenization to protect data eased my nerves. It didn't just feel like another finance tool; it was like inviting a digital financial advisor into my life.

The initial setup took about 15 minutes, and I'll admit, I cursed under my breath when one of my credit cards failed to sync immediately. The app's error message was vague—just a spinning wheel and a "retry" button that seemed to do nothing. This was my first taste of criticism: for a tool touted as seamless, this glitch felt jarring. But after a quick restart, everything clicked into place. Suddenly, I could see all my accounts in one dashboard, with real-time updates that made my old banking app look prehistoric. The technology behind it, likely leveraging open banking APIs and cloud synchronization, was impressive, even if the initial hiccup annoyed me.

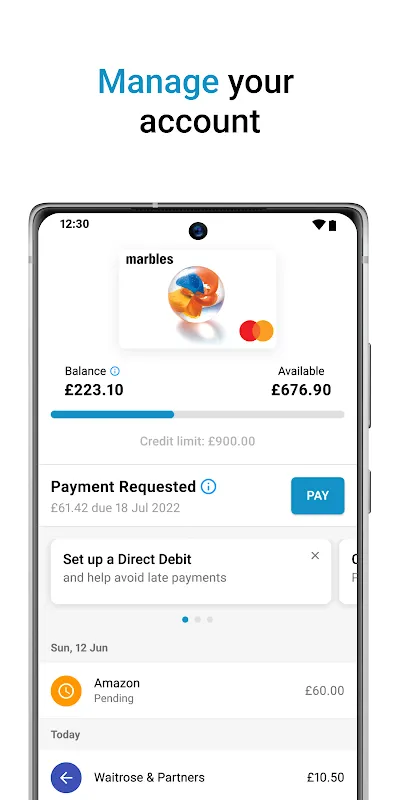

My first real test came a week later during a spontaneous shopping spree. I was browsing online for a new jacket, and as I added items to my cart, Marbles Card sent a push notification: "Budget alert: You're approaching your clothing limit for the month." It wasn't just a bland message; it was personalized, based on my spending history and categories I'd set up. I paused, checked the app, and saw a colorful pie chart breaking down my expenses. The underlying machine learning algorithms were clearly at work, analyzing patterns to offer proactive advice. In that moment, I felt a surge of empowerment—I wasn't just spending; I was making informed decisions.

But it wasn't all smooth sailing. One afternoon, I made a large purchase for a family gift, and the app's categorization feature misfired, labeling it as "dining out" instead of "gifts." I had to manually correct it, which involved tapping through multiple menus—a minor annoyance that highlighted the app's occasional rigidity. However, this flaw made me appreciate the human touch needed in fintech; no algorithm is perfect, but the ability to customize and override settings saved the day. It's these small frustrations that keep the experience real, reminding me that technology serves us, not the other way around.

The emotional rollercoaster continued when I faced an unexpected car repair bill. Normally, this would send me into a tailspin of anxiety, but with Marbles Card, I could instantly see my available funds across all accounts. I used the app's transfer feature to move money between savings and checking, all within seconds, thanks to its integration with banking networks. The relief was tangible; I paid the bill without a second thought, and the app logged the transaction immediately, updating my budget projections. It felt like having a financial co-pilot, one that didn't judge but guided with data-driven insights.

Over time, this tool became ingrained in my daily routine. I'd start my morning by glancing at the app's dashboard, which showed my net worth trending upward—a small victory that boosted my mood. The spending alerts became less about restrictions and more about mindfulness, helping me curb impulse buys. I even began using its bill reminder feature, which syncs with my calendar to avoid late fees. The technical sophistication, from secure biometric logins to predictive analytics, made me feel like I was wielding a powerful instrument, not just using an app.

There was one evening, though, that sealed my loyalty. I was traveling abroad, and my phone buzzed with a fraud alert from Marbles Card: a suspicious transaction from a foreign country. I hadn't made it, and the app's security protocols had flagged it based on unusual spending patterns. I quickly locked my card through the app and contacted my bank—all while sitting in a hotel room thousands of miles from home. The peace of mind was invaluable; it wasn't just about money management; it was about protection and trust.

Reflecting on this journey, Marbles Card hasn't just organized my finances; it's transformed my relationship with money. The highs of saving more and the lows of occasional app quirks have made it a relatable companion. It's not perfect—sometimes the notifications can be overwhelming, and I wish the UI was more intuitive in certain sections—but its core functionality is rock-solid. For anyone feeling lost in their financial chaos, this isn't a magic bullet, but it's the closest thing to a digital lifeline I've found.

Keywords: Marbles Card,news,personal finance,mobile budgeting,financial security