My Credit Prison Break with Kikoff

My Credit Prison Break with Kikoff

Rain lashed against my apartment window as I stared at the laptop screen, its glow reflecting my hollow expression. Another rejection. The words "insufficient credit history" burned into my retinas while my UberEats cart mocked me with abandoned breakfast sandwiches. That pathetic three-digit number - 523 - felt tattooed on my forehead. I couldn't even finance a damn toaster. The irony? I'd just landed my first real job with actual direct deposit. Yet there I sat, financially handcuffed, watching my new colleagues flash metal cards while I dug for bus tokens.

Tuesday nights became my financial self-flagellation ritual. Spreadsheets, budgeting apps, credit monitoring services - they all whispered the same cruel truth in sterile graphs. My thin file might as well have been written in disappearing ink. Then came the Reddit rabbit hole at 2:37 AM, bleary-eyed and desperate. Between memes and crypto bros, someone mentioned credit builder accounts. Skepticism warred with exhaustion. Another scam? But the desperation won.

Downloading Kikoff felt like reaching for a life preserver in dark waters. The onboarding surprised me - no credit check to build credit, a paradox that made me chuckle bitterly. Five bucks a month? Less than my abandoned breakfast sandwiches. I remember the tactile sensation as I dragged my thumb across the screen to authorize the first payment, the haptic buzz like a tiny jail cell door rattling open. That first month crawled by. I'd open the app compulsively, staring at the dashboard like waiting for seeds to sprout in concrete.

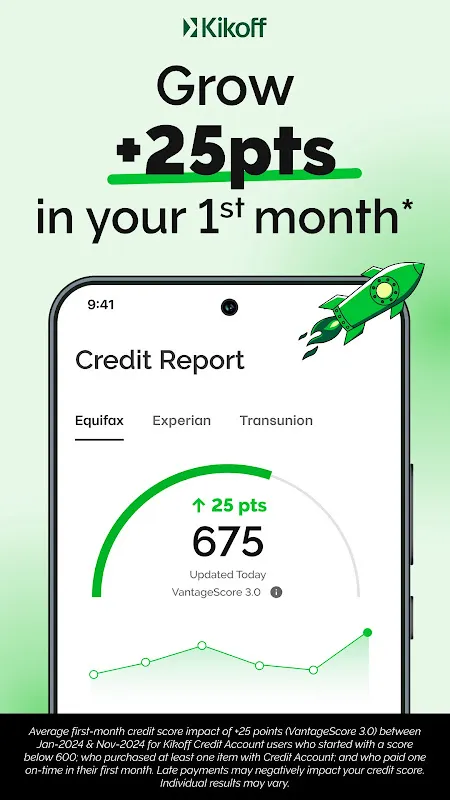

Then came the magic of auxiliary credit reporting. Unlike secured cards requiring massive deposits, Kikoff's $5 monthly fee unlocked a $750 credit line reported to all three bureaus. The engineering elegance stunned me - they'd essentially created a financial petri dish where my microscopic credit organism could safely multiply. Every on-time payment became a brick in my financial foundation, each month's report a love letter to future lenders. I started imagining my credit score like Tamagotchi, needing regular digital feeding.

Criticism? Oh absolutely. The app's Spartan design made municipal tax software look glamorous. Navigation felt like wandering through an unlit basement - functional but joyless. And that initial credit limit? Pathetic. But here's the dirty secret about financial despair - you'll cling to any branch, even if it's splintered. The brutal simplicity became its own virtue. No predatory interest rates lurking, no overdraft traps snapping shut. Just pure, unadulterated credit building stripped to its bones.

My revelation came at a Best Buy three months in. Standing before shiny laptops, I reflexively braced for rejection when applying for their card. The cashier's bored expression transformed into actual eye contact. "Approved." One word that felt like uncuffing my wrists. That night I sat in my car replaying the moment, rain pattering the roof like applause. My credit score hadn't just risen - it had staged a prison break with Kikoff as the getaway driver. The dashboard now showed 687, numbers glowing like liberation papers.

Building credit isn't about sudden windfalls. It's about the daily grind of payment reporting cycles, the invisible architecture of financial trust. Kikoff became my silent financial gym partner - no cheering, no fancy equipment, just showing up every month to lift that $5 barbell. And slowly, steadily, my financial muscles stopped trembling. Now when I tap my phone at coffee shops, it's not performative affluence but hard-won freedom. That pathetic three-digit number? It's now my six-digit salary's faithful shadow.

Keywords:Kikoff Credit Builder,news,credit rehabilitation,thin credit file,financial empowerment