My Dollars, Finally Under Control

My Dollars, Finally Under Control

Rain lashed against the coffee shop window as I stared at my third overdraft alert that month, trembling fingers gripping a lukewarm latte I couldn't afford. My phone buzzed again—$35 fee for insufficient funds. That moment crystallized my financial rock bottom: a freelance designer drowning in feast-or-famine cycles, begging clients for early payments just to cover rent. My spreadsheet "system" was a graveyard of abandoned tabs, each color-coded failure mocking my denial. Salvation came from a sleep-deprived 3 AM Google crawl—"budget apps for variable income"—where EveryDollar's promise of "zero-based budgeting" hooked me like a lifeline thrown into stormy seas.

The Setup: Facing My Money Demons

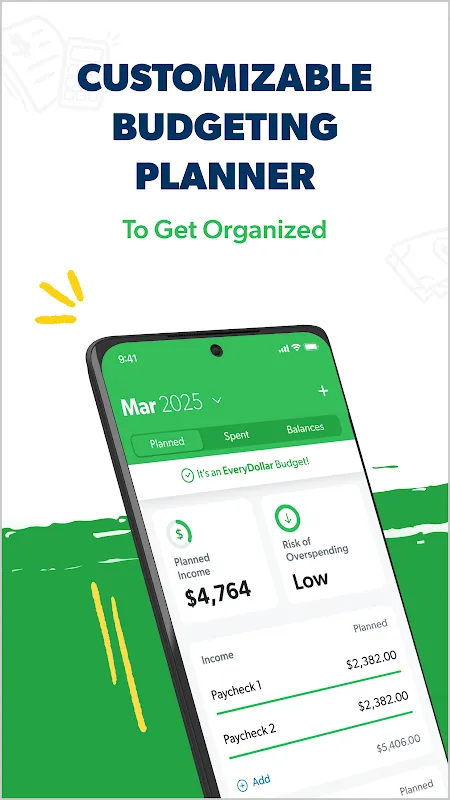

Importing bank transactions felt like performing open-heart surgery on my ego. Each swipe revealed ghosts of poor decisions: $127 for forgotten streaming services, $89 in ATM fees from cash desperation, and the brutal truth that my "emergency fund" was just $4.50 rattling in a virtual tin. Setting up categories became therapy—I created "Client Dry Spells" with a $500 buffer zone, acknowledging the instability I'd pretended didn't exist. The app forced confrontation: assigning every single dollar before the month began meant no hiding from reality. My first budget took three tear-streaked hours, but hitting "complete" flooded me with unexpected relief—like shedding a lead coat I'd worn for years.

The Turnaround: Real-Time Accountability

Game-changing moment? Standing in Target holding a $45 throw pillow, dopamine surging until I opened EveryDollar. The "Home Decor" category screamed $0 left, while my "Car Repair" fund glared red. That pillow became my symbol of reformed impulsivity—I took a photo of it abandoned on a shelf, now saved in my phone as "Wants vs. Needs Trophy." What hooked me was the frictionless tracking: whispering "coffee run, $6.80" into my phone mid-line, watching the "Eating Out" bar shrink instantly. Unlike clunky spreadsheets, transaction syncing transformed guilt into empowerment—I caught a double-billed internet charge within minutes, reclaiming $79 while the vendor still had me on hold.

Freelancer Lifeline: Riding the Income Rollercoaster

When a major client ghosted payments for six weeks, panic didn’t set in. Why? EveryDollar’s "Income Planning" section let me allocate partial payments the second they hit my account—$200 to groceries, $150 to utilities—like playing financial Tetris with falling blocks. During flush months, I’d assign bonuses to "Tax Volcano" (my nickname for quarterly payments) before temptation could strike. The app’s envelope system visualized scarcity brilliantly: watching "Fun Money" bleed to $3.27 killed more frivolous Uber Eats orders than any willpower ever could. I even created a "Psych Ward" category for impromptu therapy sessions after brutal client feedback—because mental health is non-negotiable overhead.

Not All Sunshine: Where EveryDollar Stumbles

Let’s gut-punch the flaws. The free version? A glorified notepad without bank sync—useless for impulsive mortals. I upgraded to Plus ($129/year), gritting teeth at the cost. Investment tracking is a joke; describing my Roth IRA as "Savings" feels like labeling a Ferrari "a car." And the mobile interface hates lefties—try dragging budget sliders with your right thumb while holding coffee. Worst offense? No cash tracking. My $40 farmer’s market splurge vanished into digital ether until I manually entered "MONEY ABYSS - $40" as a category. For an app preaching total control, that’s a hemorrhaging wound.

The New Rhythm: Dollars Dancing to My Beat

Eight months in, magic happens silently. I booked a Costa Rica surf trip funded entirely by my "Adventure Fund," a category born from skipped lattes. When my laptop died, I bought a replacement in cash—no credit card flop-sweat. The app’s reports revealed poetic patterns: 27% of my income went to artisanal toast in 2023 (a shame spiral I’ve since halved). True victory? Laughing at overdraft texts instead of vomiting. EveryDollar didn’t just organize my money; it rewired my scarcity brain, turning financial chaos into a waltz I now lead. Still, I side-eye its subscription fee every January—a necessary evil, like bribing a particularly effective jailer.

Keywords: EveryDollar,news,budgeting strategies,freelance finance,financial empowerment