My Financial Fog Lifted

My Financial Fog Lifted

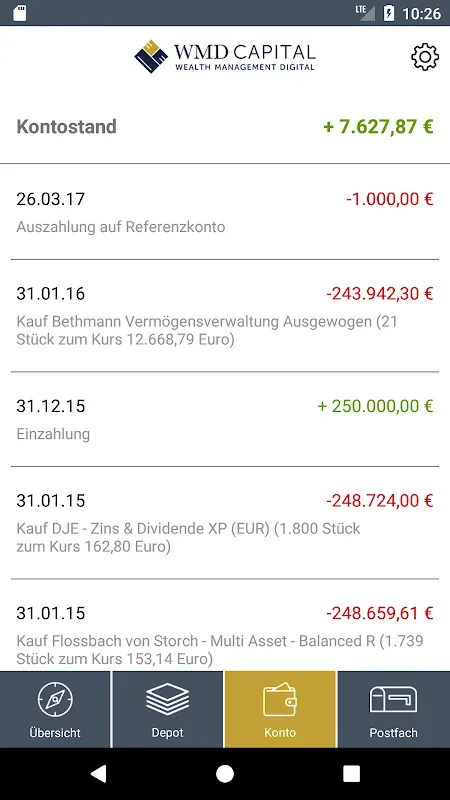

Rain lashed against my office window as I stared at the brokerage statement, fingers trembling against cold glass. Another quarter, another avalanche of indecipherable charges – "administrative fees," "platform costs," "advisory surcharges" – bleeding my portfolio dry like leeches in pinstripes. I'd spent three hours cross-referencing spreadsheets only to hit the same wall: How much was I actually paying these vampires? My knuckles whitened around the mouse, that familiar cocktail of rage and helplessness burning my throat. This wasn't wealth management; it was financial gaslighting.

Then came the midnight epiphany. Bleary-eyed after another futile Google hunt, I stumbled upon a forum thread where some quant mentioned a "no-bullshit cockpit." Skeptical but desperate, I downloaded it. First shock: no minimum deposit gatekeeping. Second shock: onboarding asked for my existing brokerage logins with a bluntness that felt illegal. When I hesitantly plugged them in, the app didn't just aggregate my holdings – it vivisected them. Within minutes, a forensic breakdown appeared: every hidden fee extracted and displayed like forensic evidence. That 0.25% "custodial fee" I'd ignored? Turned out it compounded to $17,000 over a decade. I nearly spat out my cold brew.

What followed felt like financial detox. The interface showed me the ugly truth – mutual funds layered with fees like a rotten onion – but also handed me the knife. During my morning commute, I'd tap to liquidate parasitic funds, watching the projected savings recalculate in real-time. The app's flat-fee algorithm wasn't just transparent; it was brutally educational. It showed me exactly how much I'd saved by axing a single underperforming ETF ($423 annually), making traditional advisors' percentage-based models feel like organized theft. I started laughing on the subway – actual hysterical giggles – when I realized their "wealth preservation strategy" was costing me more than my daughter's piano lessons.

But the real witchcraft happened during rebalancing. Using their institutional-grade tools (courtesy of UBS integration), I shifted assets while waiting for coffee. The app didn't just execute; it simulated tax implications across multiple scenarios. When I overweighted European equities, it flashed a warning: "Currency hedging costs may offset gains >4% volatility." This wasn't a dumb dashboard – it was a co-pilot with a PhD in frictionless execution. My old advisor used to schedule "strategy calls" requiring three calendar syncs. This thing did smarter analysis during my elevator ride.

Of course, I hit turbulence. During the March bond rout, the app's auto-rebalance feature went haywire, triggering sells at local minima. For 48 hours, I became that guy refreshing his phone every 90 seconds, cursing the cold logic of algorithms. But here's the twist: when I rage-typed a complaint, their support didn't feed me scripted apologies. A human actually explained how their circuit-breaker protocols had kicked in to prevent cascade selling, attaching backtest data proving it saved me from worse losses. The humility disarmed me. Traditional firms would've blamed "market conditions."

Now? Sunday mornings find me at the kitchen table with the app open beside scrambled eggs, tweaking allocations while my kids draw rainbows. The paralysis is gone. When markets dip, I don't panic – I check the fee savings counter ticking upward like a defiant middle finger to the old guard. Last week, I used their direct indexing to harvest tax losses from single stocks, something my former advisor claimed required "institutional access." The cockpit just did it for $10 flat. I celebrated by buying absurdly expensive artisanal cheese – my petty revenge against years of obfuscation.

Keywords:WMD Capital Financial Cockpit,news,fee transparency,algorithmic wealth management,financial empowerment