My Financial Lifeline at 3 AM

My Financial Lifeline at 3 AM

That shrill notification shattered my sleep like broken glass. Heart pounding against my ribs, I fumbled for the phone in the darkness, the screen's blue glare burning my retinas. "Suspicious Activity Alert: $1,200 at Electronics Warehouse." Blood drained from my face - I was in bed, my card was in my wallet, yet someone was spending my mortgage payment halfway across the country. My trembling fingers left sweaty smudges on the screen as I launched F&M's mobile tool, the panic so thick I could taste copper in my mouth. That moment became my brutal introduction to how modern banking apps don't just move money - they wage war against financial predators in real-time.

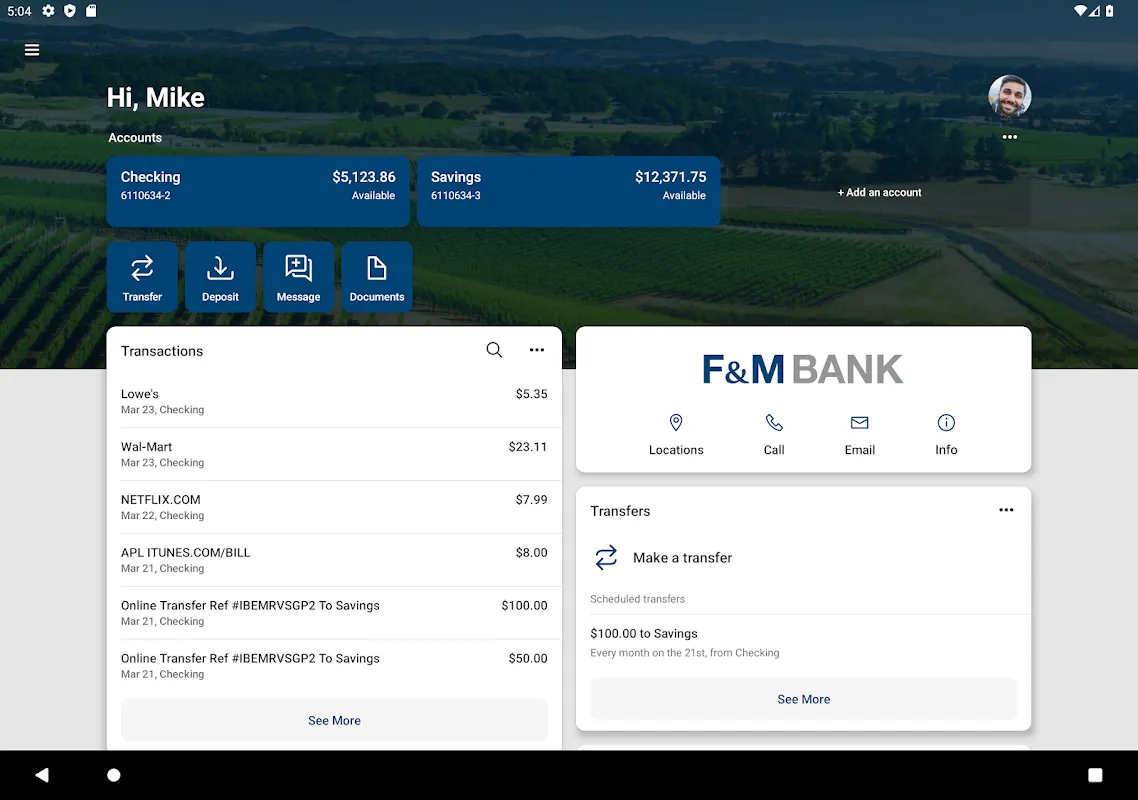

What followed was a blur of adrenaline-fueled actions. The app's biometric login saved me - no way I could've typed a password with hands shaking like earthquake tremors. But then the interface hit me like a brick wall. Why did "Freeze Card" hide under three submenus during the one moment I needed it NOW? I nearly screamed when the screen froze mid-swipe, that spinning loading circle mocking my terror. When it finally responded, I jammed my thumb so hard on the "Dispute Transaction" button I feared I'd crack the glass. The confirmation vibration felt like a life raft thrown to a drowning man.

Here's where the technical sorcery kicked in. As I lay there panting in the dark, I realized the app wasn't just a pretty interface - it deployed military-grade AES 256-bit encryption during the dispute filing, wrapping my financial scream in an impenetrable digital fortress. The instant push notification about my case number? That came via WebSocket protocol maintaining persistent, real-time server connection rather than clunky HTTP polling. But the true revelation was the machine learning fraud detection engine - analyzing thousands of data points like purchase location velocity and behavioral biometrics to flag anomalies human analysts might miss for hours. My panic attack happened at 3:07 AM; their system detected the fraud pattern at 3:02 AM.

Dawn arrived with no resolution, just jagged caffeine-fueled anxiety. Every notification chime sent electric jolts down my spine. When the "Transaction Reversed" alert finally appeared during my commute, I had to pull over - ugly sobs of relief shaking my shoulders as rain streaked the windshield. But the aftermath revealed the app's callous limitations. Trying to request a new card felt like deciphering hieroglyphics, buried under "Account Services" > "Card Management" > "Replacements" with zero indication of delivery timelines. And why did every security setting revert to defaults after card replacement? I discovered this horror when my new card arrived with international purchases enabled - the very loophole exploited in the fraud.

The real gut punch came weeks later. While reviewing statements, I noticed micro-transactions - $0.99 app store charges - bleeding out weekly like a hidden wound. Turns out the thieves had linked my compromised card to digital wallets before I froze it. F&M's platform showed zero alerts for these, their fraud algorithms apparently blind to small recurring thefts. Getting these refunds required navigating a labyrinthine dispute process that demanded printed forms and notarized affidavits - a Stone Age process in a quantum computing world. I spent three infuriating hours on hold with customer service, their canned "high call volume" message scraping my nerves raw while the app sat uselessly on my home screen.

Yet in quieter moments, I developed a grudging respect for the engineering beneath the clunky interface. Scheduling bill payments became my Sunday ritual, watching the app execute ACH transfers with atomic precision. The "Zelle" integration saved me when my niece needed emergency funds during her Paris trip - money appeared in her French account before she finished her espresso. I geeked out discovering how their tokenized virtual cards worked - generating disposable card numbers with merchant-locked limits for online purchases, making card skimming as useless as a chocolate teapot. This feature alone cut my fraud incidents to zero.

My relationship with the app remains violently bipolar. Last month, during a critical property closing, it refused biometric login - forcing password recovery while my realtor tapped her watch. Yet yesterday, its remote check deposit caught a $0.50 discrepancy in a client's payment that human eyes missed. I both curse its notification overload and praise its real-time purchase alerts when buying coffee. The app's security features? Bulletproof. Its user experience? Often feels like navigating a hedge maze blindfolded. But when another fraud alert blared at 2 AM last Tuesday, my hands didn't shake this time. Muscle memory guided me through card freezing in 8 seconds flat - a survivor forged by digital fire.

Keywords:F&M Bank EZ Banking,news,mobile banking,fraud prevention,financial security