My Financial Panic and the Digital Savior

My Financial Panic and the Digital Savior

Sweat beaded on my forehead as I stared at the broken machinery in my garage workshop. The industrial lathe—my livelihood's heartbeat—had seized mid-operation with a final metallic shriek. My mechanic's grim diagnosis: "Complete bearing failure, needs full replacement by tomorrow or you're down for weeks." The quote made my stomach drop: $8,500. Cash reserves? Drained from last month's supplier payment delays. Banks? Closed for the weekend. That familiar vise of entrepreneurial dread tightened around my chest—the terrifying calculus of lost contracts versus impossible debt.

Frantically scrolling through loan apps felt like shouting into a void. Endless forms, invasive permissions, vague timelines. Then I remembered a colleague's offhand remark about "that fintech thing with the eagle logo." Installed Poonawalla's platform with trembling fingers, half-expecting another soul-crushing dead end. The registration stunned me—no 20-page questionnaire, just ID verification via their proprietary optical recognition. It scanned my driver's license in real-time, cross-referencing databases with military-grade encryption while I filmed a 3-second video selfie. The biometric layer wasn't just security theater; it felt like a digital handshake saying, "We see you as human, not a credit score."

What happened next bordered on wizardry. Instead of generic loan offers, the interface analyzed my business transaction history—syncing securely with my cloud accounting software—and generated three tailored options. One stood out: an emergency equipment loan at 14% APR with funds released in 90 minutes if approved. I nearly choked. Traditional lenders took days for half that amount. Their risk algorithm clearly recognized the pattern—small manufacturers facing sudden CAPEX crises often rebound fastest. With nothing left to lose, I uploaded the mechanic's invoice and braced for rejection.

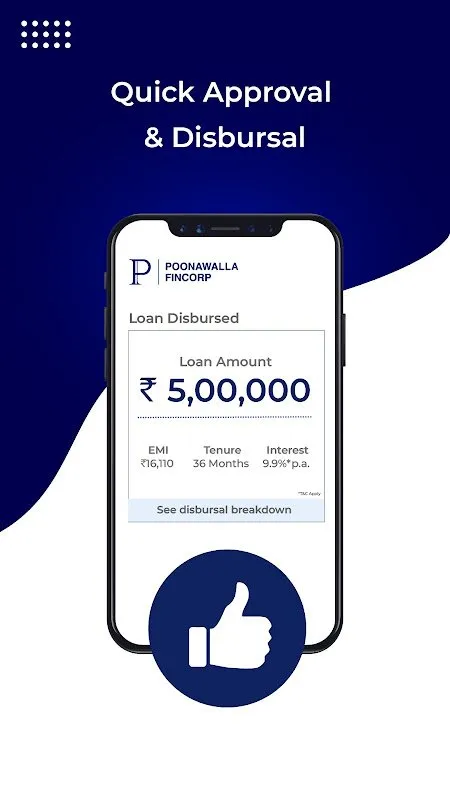

The approval notification vibrated through my phone 47 minutes later as I was literally sweeping metal shavings off the floor. No triumphant fanfare—just a clean notification: "Funds secured. Transfer initiated." When the deposit hit my account, I actually whispered "holy shit" to an empty workshop. But the real magic wasn't the speed; it was how the app transformed panic into control. The repayment dashboard visualized my cash flow impact dynamically—showing exactly how much revenue I needed daily to cover installments without crippling operations. That granular insight changed everything. Suddenly I wasn't gambling; I was strategizing.

Yet the platform wasn't flawless. Three days later, hunting for early repayment options felt like deciphering hieroglyphics. Buried under four submenus, the penalty calculator spat out conflicting figures until I rage-tapped support. Their chatbot's canned responses about "dynamic terms" felt insulting—until a human agent named Priya intervened. Her screen-share tutorial revealed hidden gesture controls: swipe left on any payment to simulate early settlements. Why wasn't this intuitive? Their backend tech sparkled while UX fundamentals stumbled. Still, Priya's quick fix saved me $217 in interest—a victory snatched from frustration's jaws.

Weeks later, I caught myself checking the app during coffee breaks. Not for loans—but for its cash flow forecasting tool. By integrating transaction data with machine learning, it predicted lean periods before they gut-punched me. When it flagged a client's likely 60-day payment delay, I adjusted inventory orders instantly. That's when this financial ally transcended crisis management. It became my fiscal sixth sense—anticipating tremors before they became quakes. The empowerment was visceral; I stopped wearing financial anxiety like a lead vest.

Tonight, as rain lashes against my garage, the lathe hums contentedly. I tap open the app just to watch real-time revenue graphs pulse upward with each finished custom bracket. The interface glows softly—a beacon in capitalism's stormiest seas. For all its occasional clunkiness, Poonawalla's ecosystem did more than save my business. It rewired my relationship with money from dread to dominion. And right now? That control feels sweeter than any profit margin.

Keywords:Poonawalla Fincorp,news,emergency funding,biometric finance,business cashflow