When My Bank Account Screamed Mercy

When My Bank Account Screamed Mercy

Sweat beaded on my forehead as the mechanic's voice crackled through the phone: "$1,200 for the transmission, payable now or your car stays." My fingers trembled clutching the cracked screen, each banking app a fresh betrayal - this one showing an overdraft fee from a forgotten streaming subscription, that one revealing my "emergency fund" had quietly bled dry. In that fluorescent-lit auto shop waiting room smelling of stale coffee and despair, financial chaos wasn't some abstract concept; it was the metallic taste of panic as I realized I couldn't distinguish necessary expenses from financial parasites sucking me dry.

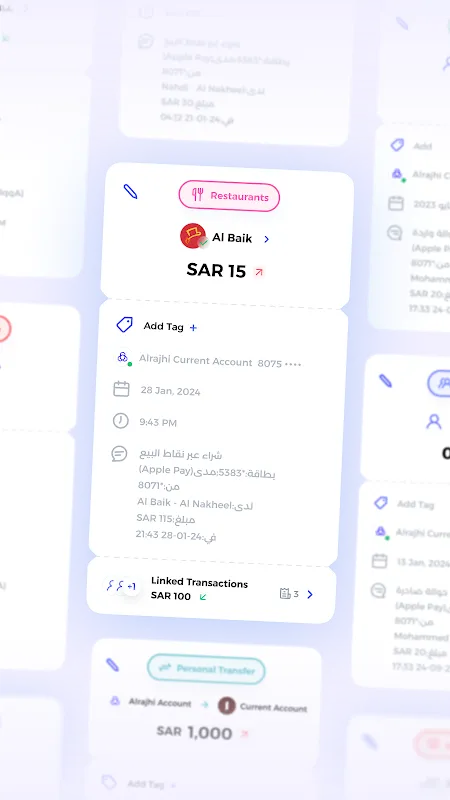

That's when Nadia slid her phone across the stained Formica table, her nail tapping a dashboard glowing with terrifying clarity. "Meet your financial exorcist," she smirked. What unfolded over the next 37 minutes rewired my relationship with money. Drahim didn't just aggregate accounts - it performed financial archaeology, unearthing recurring charges buried under transactional sediment like some digital Indiana Jones. The moment it flagged that $14.99/month "premium" weather app I'd installed during a hurricane scare three phones ago? I nearly kissed Nadia's rhinestone case. That's the dirty secret they don't tell you about financial disarray - it's not big purchases but death by a thousand $2.99 subscriptions.

The InterventionSetup felt like undressing in public. Linking accounts triggered waves of vulnerability - my retail therapy splurges, that embarrassing late-night pizza habit, the gym membership untouched since COVID. But then came the first miracle: predictive cash flow modeling based on spending rhythms. Unlike primitive budgeting apps, this beast used machine learning to recognize my freelance income's irregular heartbeat. When it projected three red alert weeks during my client's payment delay cycle, I finally understood why "savings" felt impossible. The interface became my financial confessional, each categorized transaction a whispered sin - "Entertainment: $89.50 at Brewskis Taproom" blinking accusingly in chartreuse.

Blood on the TilesInvestment features emerged like a surprise therapist. The robo-advisor didn't just allocate funds - it cross-referenced my risk tolerance quiz with actual spending trauma. Discovering it parked my first $500 in a fractional gold ETF while simultaneously killing my Starbucks habit felt like financial couples counseling. But oh, the rage when categorization glitched during Ramadan! The app saw my spike in grocery spending and assumed "hoarding behavior" rather than iftar preparations. For three furious days, it bombarded me with articles about compulsive spending until I wanted to fling my phone into the Gulf. That's when I learned the nuclear option - screaming "MISCATEGORIZED!" at the screen until the AI whimpered and recalculated.

Security became visceral during the Great Turkish Lira Incident. Attempting to invest in emerging markets triggered Drahim's paranoia protocols - a biometric gauntlet requiring facial recognition, fingerprint, and a code texted to my ancient Nokia burner phone. Annoying? Absolutely. But when I later read about regional SIM-swapping attacks targeting investment apps, that multi-layered authentication felt like finding bulletproof glass in my wallet. The encryption isn't some abstract promise - it's the satisfying "thunk" when financial vaults slam shut.

Wealth's Bitter AftertasteTrue transformation arrived via micro-investing's dark sorcery. Round-up features felt benign until I realized Drahim was weaponizing my shame. That $3.50 latte? Automatically funded a renewable energy stock slice. My impulsive Zara spree? Bought fractions of an AI company. Watching pennies from mindless spending morph into ownership stakes delivered cognitive whiplash - suddenly every swipe carried weight. The app's cruelest genius? Showing my "Latte Portfolio" outperforming my carefully researched tech stocks. Nothing crushes financial hubris like seeing your oat milk habit outsmart your MBA.

Today when market dips send colleagues into panic, I open my command center to watch diversification algorithms dance. Those colorful pie charts represent more than assets - they're battle scars from the auto shop wars. I still occasionally miss the adrenaline of financial oblivion, the thrilling irresponsibility of not knowing. But then I smell synthetic transmission fluid and feel that old panic rise. Drahim didn't just organize my money; it rewired my nervous system. Wealth isn't found in spreadsheets but in the absence of that metallic fear taste - replaced now by something far more dangerous: the quiet confidence of a general surveying conquered territory.

Keywords:Drahim,news,financial literacy,behavioral economics,open banking