GME Remit: When Panic Met Pay

GME Remit: When Panic Met Pay

Rain lashed against the taxi window as my phone buzzed like a trapped hornet. Another notification: "FINAL NOTICE - TUITION OVERDUE." Back home, my little sister's college payment was 48 hours from cancellation, and my palms left sweaty smudges on the screen. Traditional banks? A joke. Last month’s wire took five days and bled $45 in fees – enough for a week of meals here. I stared at the neon-soaked streets of this relentless city, throat tight with the acid taste of helplessness. That’s when Maria, my Spanish roommate, slammed her palm on our wobbly kitchen table. "Stop drowning in chai and download GME Remit," she barked, shoving her phone at me. "Do it now."

I’ll admit – I scoffed. Another "expat solution" promising miracles? But desperation is a brutal motivator. The download felt like admitting defeat, yet the setup shocked me. No paper forms, no branch visits. Just my passport photo snapped in dim apartment lighting and a facial scan that made me feel like a spy. Within minutes, I linked my local bank account, fingers trembling as I entered the transfer details. €1,200 to Lisbon. My thumb hovered over "Send," gut churning. What if it failed? What if the app swallowed the money whole? Maria’s eyes locked onto mine. "Trust the tech, amiga." I tapped.

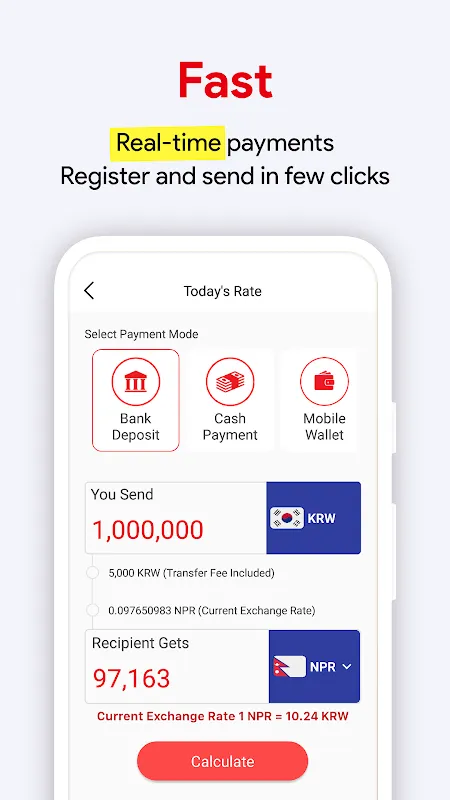

Then – magic. A green checkmark pulsed onscreen before I could exhale. Instant transfer confirmed. Not "processing," not "pending." Done. I called my sister, voice cracking. "Check the account. Now." Her scream of relief through the phone was my first real breath in hours. Later, I’d learn how they did it: direct API integration with European banks, bypassing SWIFT’s dinosaur protocols. Real-time settlement using encrypted ledger updates – no middlemen skimming time or cash. The fee? A flat €1.50. I cried into my cold chai, half-laughing at the absurdity.

But the app didn’t stop saving me. Two weeks later, racing to a job interview, I realized my transit card had vanished – again. The metro turnstile loomed like a jail door. Then I remembered GME’s transport feature. One frantic toggle in the app, and my phone morphed into a digital pass. NFC technology, same as contactless payments, synced with the city’s transit grid. I tapped my device. The gates hissed open. No plastic card, no top-up queue. Just my heartbeat slowing as the train doors closed.

Of course, it’s not all digital fairy dust. Last Tuesday, their global card feature betrayed me. Midnight online shopping spree – a rare treat – and at checkout: "DECLINED." No warning, no explanation. Turns out they’d silently flagged "luxury goods" from certain Asian retailers. A support chat yielded only bot replies for hours. I rage-slammed my laptop shut, cursing the opaque fraud algorithms. Yet when my landlord demanded rent in cash (a shady habit here), GME’s bill pay scanned his QR code instantly. The relief was physical – shoulders unlocking, jaw unclenching.

Now? I ride metros phone-first, send cash to Grandma with three taps, and sneer at brick-and-mortar banks. But the real victory isn’t the tech. It’s watching my sister’s graduation livestream, knowing I didn’t miss it because of some broken wire transfer. It’s the weightlessness when "FINANCIAL EMERGENCY" flashes on my screen now. I just open the app, breathe, and tap. Panic met its match.

Keywords:GME Remit,news,instant remittance,contactless transit,expat banking